Backtesting Stocks: How to Avoid Fooling Yourself With History

Backtesting feels like proof. You run a strategy against years of price history, the equity curve climbs, and it's tempting to treat that chart as a guarantee of future returns. It isn't. A backtest is only as honest as the assumptions baked into it — and most of the traps that cause investors to fool themselves are invisible unless you know where to look.

Here's how to run a backtest that actually tells you something useful, and how to set one up properly using Compounder's Backtest tool.

Why Backtesting Stocks Goes Wrong

The math behind a backtest is simple. The assumptions are where things fall apart.

Survivorship bias. If your test only includes companies that exist today, you've quietly excluded every company that went bankrupt, got delisted, or was acquired out of distress. A strategy that looks great over the last decade might just be a strategy that avoided disasters by accident — because the disasters aren't in your dataset anymore.

Ignoring transaction costs. Every rebalance means buying and selling. Spreads, commissions, and slippage eat into returns, and a strategy that trades monthly will feel that drag far more than one that trades yearly. Skip this cost and even a mediocre strategy can look like a market-beater on paper.

Lookahead bias. This is the subtle one. If your test uses information that wouldn't have actually been available on that historical date — like a quality score calculated with data that was later restated — you're testing against a version of history that never existed.

Overfitting. Tweak enough parameters and you'll eventually find a combination that produces a beautiful backtest. That doesn't mean you've found a real edge. It often means you've found noise that happened to line up with the past.

None of these problems mean backtesting stocks is a waste of time. They mean a backtest is only useful if it's built to resist your own optimism.

What a Realistic Test Actually Requires

A backtest worth trusting needs a few things locked down before you look at the results:

- A long enough date range. Testing over a few weeks tells you almost nothing — you need enough history to see the strategy behave across different market conditions, not just a lucky stretch.

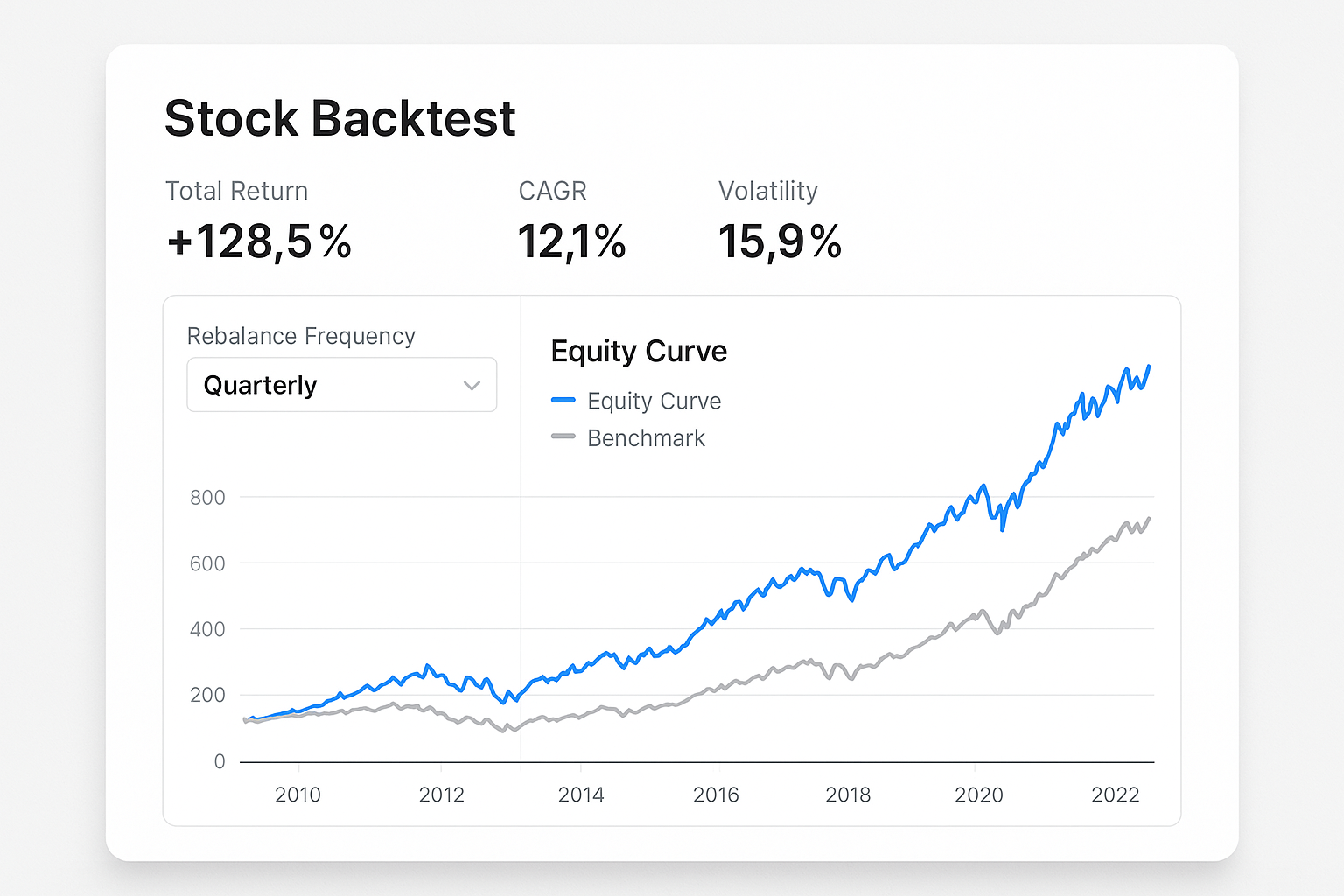

- A sensible rebalance frequency. Monthly rebalancing reacts faster to new information but multiplies transaction costs. Quarterly and yearly rebalancing trade responsiveness for lower turnover. The right choice depends on how the strategy is meant to be traded in real life — test it the way you'd actually run it.

- A defined universe. Are you testing against the top 10% of scored companies, or the top 50%? Concentrating in a smaller slice can improve or hurt returns dramatically, and it's worth testing both ends.

- A real benchmark. A strategy that returns 8% a year is meaningless without knowing what a simple index did over the same period. Always compare against a relevant benchmark, not just an absolute number.

Setting Up a Backtest in Compounder

Compounder's Backtest tool is built around these exact decisions, so you're forced to make them explicitly instead of leaving them as hidden defaults.

When you open the tool, the form on the left walks you through the setup:

- Name your test. Give it something memorable — you'll likely run several variations, and a clear name saves you from guessing later which config produced which result.

- Choose a strategy type. Pick from Compounder Score top N%, Buffett quality scoring 70+, or Graham net-net undervalued. Each represents a genuinely different philosophy — momentum-adjacent quality scoring, durable-quality investing, or deep-value net-net screening — so the choice of strategy matters as much as any other setting.

- Set your historical date range. The tool requires a minimum of 90 days, but longer ranges give you a far more reliable read on how a strategy behaves across different conditions.

- Pick a rebalance frequency. Monthly, Quarterly, or Yearly. This is where turnover and transaction cost assumptions come into play — a strategy that only wins on paper with monthly rebalancing may not survive real-world trading costs.

- Define the percentage of the universe. Decide how concentrated the test should be — testing a narrow top slice versus a broader group can change the risk profile of the results substantially.

Running the same strategy across a few different rebalance frequencies and universe sizes is one of the fastest ways to see whether a strategy has a real edge or whether the result you liked was a fluke of one specific configuration.

Turning a Backtest Into a Watchlist

Once a backtest surfaces companies or a strategy worth following more closely, don't let that insight evaporate. Anywhere you see a stock card, sector card, or theme card in Compounder — including results tied to your research — a + Follow button lets you add it to your Following list instantly. No need to navigate to the Following page first; it's a one-click way to start tracking a name the moment it catches your attention.

That matters because backtesting stocks shouldn't be a one-off exercise. The real value comes from revisiting a strategy's picks over time and watching how they actually perform going forward, not just how they performed in the past.

Keep a Record of Your Reasoning

It's easy to forget why you ran a particular test or what conclusion you reached three weeks ago. If you've been using Compounder's AI Analyst to sanity-check a strategy or dig into a specific pick, the History page keeps a running record. It has two tabs — Conversations and Deep Research — with the Conversations tab listing every chat session newest first, including the title, date last active, and message count. Click any conversation to reopen it exactly where you left off.

Pairing a disciplined backtest with a saved research trail makes it much harder to fool yourself later. You can look back at what the data showed, what you asked, and what you concluded — instead of relying on memory, which tends to remember the wins and forget the caveats.

The Takeaway

Backtesting stocks is one of the most useful things an individual investor can do — and one of the easiest ways to end up misled. Survivorship bias, ignored transaction costs, and overfitting can all turn a flawed strategy into a chart that looks like a sure thing. The fix isn't complicated: use a long enough date range, pick a rebalance frequency that matches how you'd actually trade, compare against a real benchmark, and be honest about costs. Get those inputs right, and your backtest stops being a story you tell yourself — and starts being a tool you can actually trust.